[Part 4]

Mobile Payments and the Market Potential

Mobile payments are more than another method to make purchases, it will likely emerge as the way to pay for most all your goods and services, eliminating the dependence upon carrying credit and debit cards, checks and cash. In December 2010, iSuppli released a forecast for NFC-enabled cell phones, see Figure 1F. Moreover, 13% of all cell phones shipped in 2014 will integrate NFC, up from 4.1% in 2010, according to iSuppli.

Source: iSuppli, Dec 2010

Figure 1 – Shipments of NFC-enabled Cell Phones

IMS Research expects to see an upward progression of mobile payments in mature economies, primarily as peer-to-peer transfers and for completion of online purchases. It sees the greatest growth in “unbanked” transactions in African and Asian countries using SMS. Today, SMS is the dominate medium for conducting transactions; however, the mobile payment market (in general) will use both SMS and contactless methods and is projected to account for 140 billion transactions in 2015G.

Contactless payments which have been in use since the 1980s have paved the way for NFC-enabled cell phone payments (i.e. mobile payments). Contactless payment studies have been carried out in fast-food restaurants, cafeterias and transit authorities in North America and European for a number of yearsH,I,J. Pilot programs in North America and Europe have shown that:

• Contactless payments cut the average transaction time in half

• Contactless payments reduce the transaction time relative to a cash transaction

• Contactless payments are about five times faster than card payments requiring a signature

In these pilot programs, mobile purchases have taken place using a variety of contactless devices – prepaid contactless stickers, key fobs and cards. These pilot programs have helped to further develop the NFC-enabled mobile phone model. Similar to a card payment, to finalize the NFC transaction the user simply enters a short personal security code (i.e. personal identification number, PIN), and then touches their phone to the terminal for confirmation.

Once the transaction is complete, the phone’s purchasing capability is secured and locked so no further transaction takes place unless re-initiated. This means that if you lose your phone, nobody would be able to use that mobile device to make unauthorized purchases. This provides an essential higher-level of security compared to credit cards or other payment methods that typically reside in a physical wallet. The payment transaction is then processed in the conventional way as a regular credit card. A general credit card transaction process is shown in Figure 2.

Figure 2 – General Credit Card Transaction Process

Once the credit card transaction goes through – funds are transferred from the customer’s bank to the merchant’s bank. Banks and credit card companies then share a “cost of transaction” fee called an Interchange Fee.

Figure 3 shows an example of how the present credit card fee model dsitributes a $100 purchase amongst the present ecosystem stakeholders. This is a general model and actual fee amounts may differ between banks, credit card processors and merchants. The credit card transaction fee has been part of the financial transaction process since the national credit card system was formed and will continue after NFC-enabled devices enter into the model.

Figure 3 – Distribution of Interchange Fee

Once the NFC-enabled phone is included in the transaction process, the carrier and a trusted service manager (TSM) are two additional stakeholders added in the transaction processing loop, see Figure 4. An NFC-enabled phone behaves just like a credit card; however, with the NFC-enabled phone over-the-air (OTA) updates are possible and all service providers (in general) in the transaction process may find other revenue generating opportunities that add value.

On the merchant side of the transaction process, the POS terminal is equipped with an NFC chip reader. When the NFC-enabled phone touches the contactless terminal, the terminal is able to pull essential personal identification and account information from the phone, similar to the data contained on the magnetic stripe of a credit or debit card. Because mobile devices will be provisioned with several payment accounts, the phone owner can choose which account to debit the cost of the purchase.

The phone owner may select from the eWallet, a credit or debit card account, or a merchant-specific ”stored value account” – something like a refillable gift card. Because commerce-enabled mobile devices can manage multiple accounts via the eWallet as well as receive OTA updates, this capability puts merchant-sponsored prepayment incentive programs on the same level as major credit and debit cards from the customer’s usability perspective. And that opens new opportunities for merchants to directly build customer loyalty and possibly even lower their (i.e. merchant’s) transaction costs.

Figure 4 – Credit Card Transaction Process with NFC Mobile Payments

Because NFC-enabled phone transactions generally do not change the transaction process for the consumer, it should be easier for the consumer to adopt the technology, thus lowering the learning curve. This transaction has implications for the entire mobile commerce value chain, which includes merchants, POS equipment manufacturers, financial entities, transaction processors, mobile phone manufacturers and carriers.

It opens the door for new entities to enter into the transaction process and additional fees to be garnered. Figure 5 describes the additional fees that could result from the inclusion of a (NFC) mobile payment.

Figure 5 – Proposed Monetary Flow After NFC Mobile Payments Is Introduced

Mobile commerce, or m-commerce, offers significant revenue opportunities (for the entity/ies that accept the TSM role) in the form of provisioning costs and potentially higher-priced data plans to customers. Revenue from advertising carried over the network and additional revenue from transactions are part of the new model as NFC-based phones become available. As the financial transaction process has gone through a number of phases, its “value proposition” has evolved, increasing the opportunity for mobile commerce services, as described below:

Phases in the Financial Transaction Process

• Phase 1: Plastic card/magnetic stripe

• Phase 2: Contactless payments using NFC chip in plastic card

• Phase 3: NFC mobile payments, advertising and promotions

Value Propositions

• Value proposition of Phase 1:

o Convenience

o Alternative to carrying cash

• Value proposition of Phase 2:

o Replaces cash faster

o Moves lines faster

o First step towards alternative payment option

o Increased customer loyalty

o Added security

• Value proposition of Phase 3 (in addition to phase 2):

o Higher usage of (digital) cards

o Low cost alternative payment options

o New customer acquisitions

o Highly efficient promotion programs

o Targeted coupon issuance and redemption

o Tailored product and services information dissemination

Carriers have an opportunity to be the first mover, or lead, in this NFC-enabled phone market. A key financial measure for carriers is Average Revenue Per User (ARPU), which is the overall revenue divided by total number of users. A fundamental business strategy for carriers is to increase ARPU, and mobile commerce provides an opportunity to do just that.

As the financial transaction process matures from Phase 2 into Phase 3, so does the evolution of several possible ecosystem models that illustrate the administration of the OTA information and role of the TSM. Each model would be based on the geographic location of the service, and as the models evolve so will the opportunity to increase the ARPU. The carriers, handset OEMs (e.g. Apple, RIM and Motorola) and financial institutions, may have a mixed role in managing the transaction. Three possibilities are:

• Self-managed: Carriers, financial institutions and OEMs will self-administer their NFC trusted services

• Cooperative: Other carriers, financial institutions and OEMs will outsource their NFC trusted services to an existing or new ecosystem players

• A developed NFC environment: Carriers and OEMs will outsource some of their NFC trusted services to multiple ecosystem experts

Because carriers provide the wireless link to the handset owner, they also have a greater influence in determining how the additional revenue is generated and shared. There are several vital questions to consider: what new services form the basis of NFC business model revenues, and will mobile commerce increase ARPU enough to offset the added cost of NFC-enabled handsets? The following is a list of new services to that could generate additional ARPU:

• Provisioning – fees per download

o Secure download of credit, debit, prepaid, loyalty, tickets, transit

• Card Services – fees per event/action

o Such as lost and stolen management

§ Remote card deletion when lost phone is reported

§ Re-issuance to new phones

o Reissuance on card expiration

• One-to-One Marketing – OTA postage fees

o Personalized coupons, promotions, rewards, and advertising

• Smart Posters – data air-time fees

o Content delivery based on user tapping NFC-enabled (smart) posters

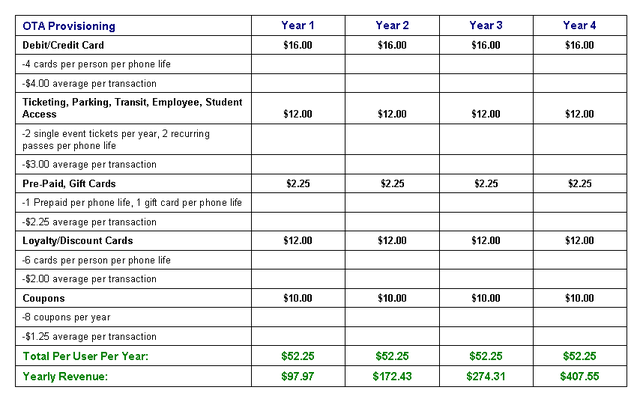

The “increased ARPU” value is somewhat unknown because until mobile commerce catches on – becomes “sticky” – a percentage of those mobile devices purchased probably will not be activated for mobile commerce and therefore won’t help raise ARPU immediately. Financial entities pay fees to have their cards and coupons activated – Existing Solution Fees – in Table 1. Now carriers (and TSMs) could use OTA provisioning as the vehicle that drives the additional (delta) ARPU by charging more for card and coupon activation. Costs in this model are estimates:

Source: Various sources from Internet

Table 1 – Estimated Costs for OTA Provisioning

The categories in Table 1 are the “most likely” categories that reflect the present use cases for non-cash or non-check (i.e. credit or debit card) transactions. And as mobile payments mature and become the norm with consumers and prosumers in the coming years, other or new categories will also become valuable ARPU drivers.

For the above categories and their given cost assumptions, to determine the total yearly revenue derived from OTA provisioning, the user base of NFC-enabled phones along with their enablement and utilization should be considered. Table 2 reflects the calculation for Years 1 through 4, as the number of subscribers, enablement and utilization grows.

Source: Various sources from Internet

Table 2 – Estimated Revenue for OTA Provisioning

Table 3 depicts the Delta Yearly Revenue. There is potentially over $206 million in additional revenue in Year 4 with a NFC user base of 7.2 million (60M Subscribers x 30% NFC Enablement in Phones x 40% Consumer Utilization).

Source: Various sources from Internet

Table 3 – Delta (Increase) in Estimated Revenue using OTA Provisioning

Assumptions (2 year phone life-cycle) for Tables 2 and 3:

Year 1: 50M subscribers, 15% NFC Enablement in Phones, 25% Consumer Utilization

Year 2: 55M subscribers, 20% NFC Enablement in Phones, 30% Consumer Utilization

Year 3: 60M subscribers, 25% NFC Enablement in Phones, 35% Consumer Utilization

Year 4: 60M subscribers, 30% NFC Enablement in Phones, 40% Consumer Utilization

As mentioned, new categories will become relevant as the market matures. Here is a short list of new categories to consider:

• Employee/Student badge

• One-to-One marketing

• New NFC-enabled applications

By including the new categories in the calculation for ARPU revenue, see Table 4, the additional revenue garnered could grow to over $100 million in Year 4.

Source: Various sources from Internet

Table 4 – Estimated Revenue using OTA Provisioning + New Category Revenue

Comparing Table 5 and Table 3 shows that the Delta Yearly Revenue plus New Categories Revenue could grow to over $308 million in Year 4, up from about $206 million, for a NFC user base of 7.2 million (60M Subscribers x 30% NFC Enablement in Phones x 40% Consumer Utilization).

Source: Various sources from Internet

Table 5 - Delta (Increase) in Est. Revenue using OTA Provisioning + New Categories

Assumptions (2 year phone life-cycle) for Tables 4 and 5:

Year 1: 50M subscribers, 15% NFC Enablement in Phones, 25% Consumer Utilization

Year 2: 55M subscribers, 20% NFC Enablement in Phones, 30% Consumer Utilization

Year 3: 60M subscribers, 25% NFC Enablement in Phones, 35% Consumer Utilization

Year 4: 60M subscribers, 30% NFC Enablement in Phones, 40% Consumer Utilization

It is clear that the incentive for carriers to develop and launch NFC-enabled services can provide additional ARPU. This is just one model and other categories, fees, number of users/subscribers, and NFC enablement and utilization will vary for other models. Since carriers could generate additional ARPU, will merchants, banks and credit card companies also benefit, either directly through increased transactions and transaction efficiency, or in the sharing of revenue by the carriers? All stakeholders will benefit from NFC-enabled mobile payments and a revenue distribution model will develop as the ecosystem evolves. For the NFC-based mobile payment market to thrive, however, merchants need to install contactless terminals.

Contactless payment terminals present a somewhat different challenge for merchants. Although they are not significantly different in cost compared to standard credit or debit card readers, traditional card readers cannot be retrofitted with NFC capability, which means that merchants will need to invest in new equipment to support mobile purchases.

IMS Research predicts that the number of locations worldwide accepting contactless payments will grow to over 12.5 million by the end of 2013. Figure 6 shows an estimated growth of NFC-enabled POS terminals relative to non-NFC POS terminals through 2013 (in North America only). There are presently about 600,000 contactless POS terminals and about 13 million non-contactless POS terminals at merchant stores – an installed base of about 13.6 million (at end of 2009).

Source: Various sources from Internet

Figure 6 – POS Terminals in North America

By end of 2013, there are estimated to be nearly 3.6 million contactless terminals and about 11 million non-contactless terminals at merchant stores – an installed base of nearly 14.6 million. Figure 6 shows growth in the total number of installed terminals of about 1 million over four (4) years, and about 2.9 million contactless terminals will be added in that same period.

Higher-end contactless terminals that allow the consumer to swipe or tap their cards or mobile devices, enter their PIN or signature, respond to prompts and be exposed to real-time offers and promotions through its LCD display typically cost about $550 each. Lower-end contactless terminals typically cost about $350. The cost for installing new terminals by the merchant isn’t high and shouldn’t be a barrier.

However, the lack of incentive or initiation by merchants to more aggressively upgrade to contactless terminals could change as more and more consumers begin using NFC-enabled phones (as well as contactless cards).

Which merchants are inclined to upgrade sooner than later? There are three levels of merchants, with a tiered breakdown of each merchant shown in Figure 7. The numbers are taken from Figure 6 and further specified. Tier 1, Tier 2, and Tier 3 categories are defined as:

Tier 1 locations are nationwide companies - Target, Walmart, Starbucks, McDonalds, etc

Tier 2 locations are more regional companies - Jack in the Box, Foster Freeze, etc

Tier 3 locations are smaller businesses - Neighborhood dry cleaner, taxis, etc

Source: Various sources from Internet

Figure 7 – POS Terminals in North America by Merchant Category

Each Tier will have approximately the same absolute growth over the next several years as merchants choose to upgrade to contactless payment terminals and new enterprises open for business. It’s not difficult, however, for merchants to recover this investment.

Because mobile transactions are faster than cash or card transactions (as mentioned above), more customers are processed (e.g. move through the checkout lane) in a given period of time, raising the operational efficiency of the business. Why haven’t more merchants been interested in upgrading to contactless payment terminals to take advantage of the contactless cards (installed based), and will they upgrade once the upcoming new NFC-enabled phones become available?

A barrier could be cost – there is some premium for an NFC-enabled payment terminal. Another possibility it that most merchants who understand the technology have already started to use it, or there isn’t a need to reduce the queue time to speed the transaction. Also, at this time the majority of merchants may not see enough customer demand (or requests) to use a contactless card, something the credit card companies can be more proactive to promote. Optimistically, NFC-enabled phones will change that circumstance.

As the benefits to consumers become evident through aggressive (gorilla) marketing and promotional campaigns by terminal suppliers, carriers and financial institutions, in time the rate of adoption of (both attended and unattended) contactless terminals will increase, exceeding the present market forecast.

As mobile payments rollout globally, the role of managing the accounts and OTA updates will become more important. The role that provides this breadth of account management service for mobile devices is more involved than traditional credit and debit card processing. And many of the stakeholders in the mobile commerce ecosystem want to control that role. Ideally, the candidate for fulfilling the role may be an entity (or entities) with relationships to financial institutions, handset manufactures and carriers, or some combination there of.

In North America, the ISIS joint venture may be the answer to this pending quandary – they’ve pulled together the key partners who have experience in contactless payments and who can contribute to managing the mobile commerce ecosystem. In Japan Europe has a number of other TSM-oriented suitors: Gemalto, Obethur Technologies and Zapa Technology, to name a few.

The NFC Forum released a white paper in 2008 that describes the NFC ecosystem and the need and benefits for a TSM. A partnership that is comprised of the key stakeholders should determine and facilitate the cell phone-enabled NFC transaction process so it works smoothly and seamlessly. There are many options, and as the mobile payment ecosystem matures, so will the TSM role and the addition (and sharing) of revenue generating services.

Your index chart show your business (quality of product)

ReplyDeletePlastic CardS

Architecture design services in Dubai

ReplyDeleteInterior design services in Dubai

This comment has been removed by the author.

ReplyDeleteUtilizing even some of the uncomplicated strategies like searching somebody's title on the search engines you could be capable of finding anyone. Considering that a larger share of World wide web users want to utilize Google for lookups this process USA Search People is now referred to as "Googling" someone. Initially this search was referred to as a random look instead of a good way of defining men and women rapidly and cost-free.

ReplyDeleteRIBS Technologies offers the best contactless business card and is renowned as a leading provider of digital business card solutions.

ReplyDeleteRIBS Technologies stands out as the go-to company for customizable NFC business card. Clients have the flexibility to personalize their cards with unique designs, logos, and contact information, ensuring a professional and memorable representation of their brand.