[Part 6]

Perspective

The credit card companies – MasterCard, Visa, and Europay (originally know as: EMV) as well as American Express and Diners Club – and their early involvement with smart cards to create its specification, have helped to guide the way for contactless payments. EMVCo was established to oversee long-term maintenance and compatible of the system. With the exception of countries such as the United States

Contactless payment terminals are increasingly available at merchant locations (e.g. McDonald’s, company cafeterias), transit ticketing (e.g. train and bus terminals) and unattended locations (e.g. vending machines). Payment terminal manufacturers are seeing an increase in the rate of contactless terminal sales (e.g. high-end terminals that have displays with in-store personalized mobile marketing capabilities), while credit card companies are seeing an increase in use of contactless cards and alternative devices (e.g. key fobs).

Carriers who have rolled out mobile contactless proximity payment trials to date have clearly benefited from the ability to leverage the contactless infrastructure that already exists in many regions of the world, due to the success of contactless payment deployments which utilized a variety of form factors, including cards and attachable /programmable stickers.

Handset manufacturers are beginning to recognize the value proposition of NFC-enabled phones and are introducing many Smartphones with NFC beginning in 2011. The ISIS JV (a trademark of JVL Ventures, LLC) has been formed to deliver/launch a mobile payment system in North America into key geographic markets over the next 15 to 18 months. Europe and other regions (globally) have rolled out their mobile payments system and are beginning to upgrade (e.g. Japan

In addition to the confluence of available/usable contactless payment technologies and stakeholders collaborating with a common interest both with trials and actual deployments, the various factors driving the business case to include NFC technology in mobile devices can be summarized:

• The ubiquity of the mobile phone, and more specifically, the Smartphone

• The capacity for extended functionality of the handset now that more Smartphones are in the hands of consumers and prosumers

• The continued increase in the number of contactless cards and contactless payment terminals

• The continued increase in the use of mobile phones for transactions, e.g. SMS

• Carriers, banks, credit card processing companies and handset manufacturers in North America have realized that now is the time to combine forces and drive the ecosystem for mobile payments

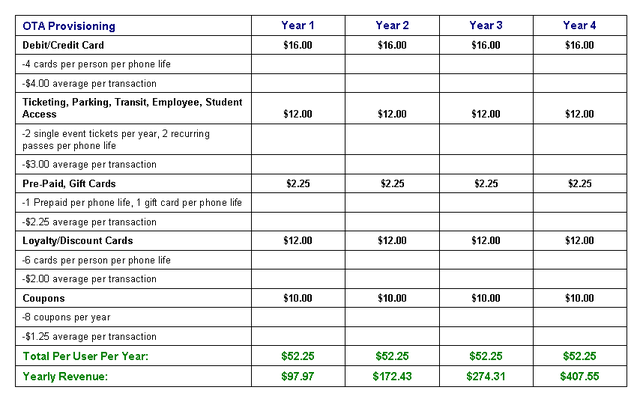

• Additional revenue can be gained through OTA provisioning and eWallet advertising

For the consumer and prosumer, mobile payments have a compelling value proposition – secure payments, flexibility and convenience. However, “mobile payments” isn’t for everybody and consumers that find “change” difficult, will less likely integrate this technology into their lives.

Purchasers of goods and services that have a Smartphone (or other advanced mobile technology), would be more inclined to utilize this payment vehicle since these Smartphone owners usually are Innovators, Early Adopters and Early Majority (as described by marketing terminology). The product diffusion curve in Figure 9 depicts the penetration of a product as a percentage of people. People are defined as: those who own and use (even if it’s only on occasion) a “cell phone”; and Smartphone is a category within cell phones.

As time advances so does the penetration of a (new) product or technology as more people use it. The curve can be used as an illustration for personality types that would have a greater (and lesser) tendency to use (i.e. buy and implement in their life style) the product: greater tendency – Innovators, and lesser tendency – Laggards.

Moreover, not all Innovators who embrace a new product, e.g. a Smartphone, would be equally as quick to embrace a new technology subset of that product, e.g. mobile payments using NFC technology. In other words, a portion of Early Adopters may be Innovators or Early Majority when it comes to actually using their Smartphone’s NFC technology for mobile payments; which is example of NFC utilization and enablement (as earlier described) as a percentage of subscribers.

Figure 9 – Product Diffusion Curve

There are a myriad of papers written on the psychology of habit adoption, but a study conducted by the Boston Federal Reserve in 2007 on Consumer Behavior and Payment Choice may provide some insight into barriers as well as decisions behind adoption. This study used employees of the Fed, so the results in terms of percentages may be more conservative in comparison to the general population. However, the reasons and thoughts behind the choices for using cash, checks, debit or credit cards to paid bills or buy goods does have validity. A couple of interesting facts include:

• Cost, convenience, and timing are the three most important fundamental characteristics that determine consumers’ adoption and use of a payment method

• Safety and privacy also are important as they relate to susceptibility / consequences of identity theft

• Payment method; as most consumers use a variety of payment methods each month for each type of bill

• Payment choice is a joint decision (between couples)

When consumers switched from checks to other payment methods, the method they chose depended on the location and amount of the payment, among other things.

1. For payment amounts below $20 (also called micro payments), 51% used cash

2. For medium-sized payments ($20–50), 46% used debit cards

3. For large payments (amounts above $50), 48% used credit cards

The study further discusses as to why respondents change payment methods:

• About 37% of respondents reported that convenience and various elements of cost were the primary influences on their decisions to substitute electronic payments for check

• 18% of responses stated that cost (i.e. saving money on checks) was a factor

• 13% of responses indicated that better recordkeeping was a factor in respondents’ switching (from checks to debit cards)

• Almost one-third (~33%) of responses indicated that use of debit cards increased because more stores accepted them than previously

This last sentence can also describe why and how barriers could have been lowered earlier – by implementing electronic payment terminals at the retail stores. More specifically, if merchants installed only NFC-enabled terminals with mag-stripe capabilities and credit card companies issued more contactless credit/debit cards, then this push mechanism could drive consumers to transition their payment habits more quickly, thus penetrating the product diffusion curve faster. (Personally, I don’t recall ever being asked by my credit card companies if I wanted a contactless-enabled credit or debit card.) Once NFC-enabled phones become readily-available, consumers will have other payment options then to use a contactless terminal for a transaction.

Two NFC-enabled phones using the peer-to-peer mode – one in Active (or Reader) mode and the other in Passive (or Tag) mode – can transact with each other without the need for a contactless terminal as the point of interaction (POI). This can open the market for new types of transacting that bypass the present contactless terminal system. Virtual and mobile merchants, for example, would be able to offer discounts, their own loyalty cards and accept payments – phone to phone – using the OTA provisioning to finalize the transaction.

In addition, a user could pay their bills from their eWallet, transfer funds from saving to checking, transfer balances from credit card to credit card, and transfer funds to a relative across the country – rather than using Western Union ! The one-to-one transaction feature could further motivate the phone owner to start using mobile payments as a vehicle for making financial transactions. Whether the transaction is made peer-to-peer or through a contactless terminal, it’s safe and secure. Mobile payments security, and the capability of preventing someone from hacking or accessing your eWallet information, is greater than with a credit card or check book.

OTA “remote access” software used by companies on employee’s laptops to access it and lock out a third-party from retrieving the files is similar in capability as the software used on a company-issued mobile phone. This security software capability is presently available and is used to secure the eWallet, creating several barriers to access.

If your mobile phone is lost or stolen, a PIN number (i.e. barrier #1) prevents a third-party from accessing your eWallet. “Three tries and you’re out” feature (barrier #2) could also be included as a means to lock down the eWallet when the PIN is incorrectly entered. As biometrics becomes more available and reliable, a fingerprint scan, iris scan or retinal scan (barrier #3) can be also used to prevent unwanted access to your eWallet. Further, OTA provisioning will give the mobile phone owner the ability to send an SMS or go online and enter a “remote swipe” code (barrier #4). This code can be sent to the handset via the cellular network and/or Internet (accessible via Wi-Fi), so when the mobile phone is “on” all eWallet data will be automatically deleted or “cleaned” from it. Whether the phone is “on” or “off”, however, and the battery or SIM is attempted to be removed, a “local swipe” to the eWallet can be automatically executed (barrier #5), thwarting the intruder.

Since all information is backed up automatically to an off-phone or cloud-based storage, when you buy a new mobile phone or find the old one, the eWallet information can be re-downloaded to the phone through OTA provisioning. With all Smartphones having built-in GPS, apps exist (see AptoLink) that can run in the background and can track (and upload) its location so a lost or stolen phone can be quickly traced. This functionality may be the first line of defense, since many phones are merely “temporarily lost” or misplaced. GPS can be used for more than just tracking a phone’s location.

GPS will become more valuable, however, as a tool for location-based services (LBS), primarily advertising to the handset with information that is geo-based and habit-based. With the understanding of a person’s buying habits that are based on location/day/time-of-day, over time an efficient notification, advertising and coupon offering can be provided without spamming. This functionality is a complement to mobile payments – by assisting a phone owner to make a purchase based on location and habit, then using your handset to complete the financial transaction, wirelessly.

NFC mobile payment technology is safe and secure for consumers to use whether it’s finding the phone’s location (lost or stolen), having remote access to delete all eWallet data, or efficient advertising based on location/habit-based activities. Some additional thoughts on moving the consumer towards adopting NFC technology include:

1. Make the process simple, secure and effortless

2. Do the work for the handset owner – don’t ask the handset owner to fill out streams of paper work and re-enter all credit, debit and loyalty card information

3. Prefill-out the phone owner’s confidential information and have them OK a simple and concise “list” online

4. Securely provision their information in a way that the phone owner only has to accept each digital application (with the prefilled-out information) on their eWallet

5. Simple editing should be available on the eWallet if previously reviewed information online isn’t fully accurate or needs to be updated on-the-fly

NFC-enabled mobile payment has the financial infrastructure in place. Stakeholders have conducted trials globally for a number of years and are now moving forward and pulling together complementary partnerships. Japan

References

A – Mobile Payment - Advanced Technologies (NFC), Strategies And Future Of Remote & Proximity Payment In U.S., Aug 26, 2010, http://www.pymnts.com/research-and-markets-mobile-payment---advanced-technologies-nfc-strategies-and-future-of-remote--proximity-payment-in-us-20100816005641/

B – Nokia, Philips and Sony establish the Near Field Communication (NFC) Forum, http://www.nxp.com/news/content/file_1053.html

C – Radio Frequency Identification Technology History, http://en.wikipedia.org/wiki/Radio-frequency_identification

D – Smart Card Technology History, http://www.smartcardalliance.org/

E – Smart Card History, http://en.wikipedia.org/wiki/Smart_card

F – Cell Phone Mobile Payment Market Set for Take Off, Dec 20 2010, http://www.isuppli.com/Mobile-and-Wireless-Communications/News/Pages/Cell-Phone-Mobile-Payment-Market-Set-for-Take-Off.aspx

G – Mobile Wallet Users Forecast To Reach 800 Million in 2015

Date: 29 June 2010, http://imsresearch.com/news-events/press-template.php?pr_id=1474&cat_id=169&from

Date: 29 June 2010, http://imsresearch.com/news-events/press-template.php?pr_id=1474&cat_id=169&from

H - Cingular Starts NFC Trials in the USA

I – Trains and burgers: Sprint launching NFC trial in Bay Area, http://mobile.engadget.com/2007/12/21/trains-and-burgers-sprint-launching-nfc-trial-in-bay-area/

J – Digital Wallets at the Ready in NYC for Visa's Latest Trials, http://gizmodo.com/5617754/digital-wallets-at-the-ready-in-nyc-for-visas-latest-trials

K – Proximity Mobile Payments: Leveraging NFC and the Contactless Financial Payments Infrastructure, http://www.sunildewan.com/uploads/Proximity_Mobile_Payments_Leveraging_NFC_and_Contactless_Financial.pdf